Introduction

Debt is one of the most common financial challenges faced by individuals, families, and even successful professionals. It often builds quietly—through credit cards, loans, lifestyle inflation, or unexpected life events—until it begins to limit choices, increase stress, and reduce long-term opportunities.

If you are asking, “How can I get out of debt?”, you are already taking the most important step: awareness.

Getting out of debt is not about punishment, extreme frugality, or quick fixes. It is about strategy, structure, and disciplined execution. Just as organizations recover from financial setbacks through planning and leadership, individuals can regain control through clear systems and intentional decisions.

This article presents a CEO-friendly approach to debt elimination—focused on clarity, sustainability, and long-term stability rather than emotional reactions or unrealistic promises.

Reframing Debt as a Management Problem

Debt Is a System Issue, Not a Moral Failure

Debt is rarely the result of a single bad decision. More often, it develops due to:

- Cash-flow mismatches

- Overreliance on credit

- Lack of financial visibility

- Life disruptions such as illness, job loss, or emergencies

From a leadership perspective, debt is a system failure, not a character flaw. And system problems can be fixed.

Productive vs. Destructive Debt

Not all debt is equal.

Productive debt may:

- Increase earning potential

- Support long-term growth

- Be structured with manageable terms

Destructive debt typically:

- Funds consumption

- Carries high interest rates

- Grows faster than income

- Limits future flexibility

Getting out of debt starts with identifying which obligations no longer serve a strategic purpose.

Why Getting Out of Debt Matters

Restoring Financial Optionality

Debt reduces options. High monthly payments:

- Limit career or business choices

- Reduce savings capacity

- Increase vulnerability to disruptions

Eliminating debt increases flexibility—one of the most valuable assets in both business and personal finance.

Improving Mental Clarity and Decision Quality

Financial pressure affects how decisions are made. Chronic debt stress often leads to:

- Short-term thinking

- Avoidance behavior

- Emotional spending

Reducing debt restores clarity, confidence, and control.

Creating the Foundation for Wealth Building

Debt works against compounding. Savings and investments work with it.

Before wealth can grow sustainably, financial leaks must be closed.

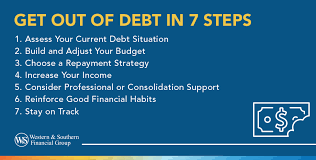

Step One: Get Full Financial Visibility

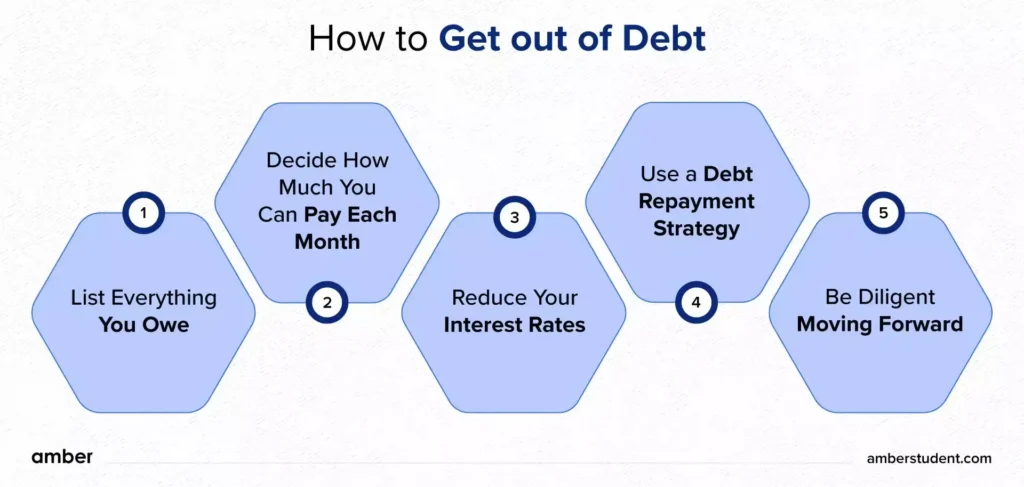

Conduct a Debt Inventory

Start with facts, not assumptions. List:

- Each debt

- Total balance

- Interest rate

- Minimum payment

- Due date

Avoid judgment. This is an operational audit, not a performance review.

Analyze Cash Flow

Debt elimination depends on cash flow, not income alone.

Understand:

- Net monthly income

- Fixed expenses

- Variable spending

- Discretionary costs

Clarity reveals leverage points.

Step Two: Define a Clear Debt-Exit Objective

Vague Goals Do Not Produce Results

“Getting out of debt” is not a strategy.

Effective goals are:

- Specific

- Measurable

- Time-bound

Examples:

- Eliminate all high-interest debt within 18 months

- Reduce total debt by 50% in two years

- Become consumer-debt-free by a specific date

Clear objectives guide consistent action.

Align Goals With Life Priorities

Debt reduction should support broader goals:

- Career growth

- Family stability

- Business development

- Health and well-being

A strategy that ignores human realities is unsustainable.

Step Three: Choose a Debt Reduction Strategy

The Snowball Method

This approach prioritizes paying off the smallest balances first.

Advantages:

- Faster early wins

- Increased motivation

- Behavioral momentum

Best for individuals who benefit from visible progress.

The Avalanche Method

This strategy focuses on debts with the highest interest rates first.

Advantages:

- Minimizes total interest paid

- More efficient mathematically

- Faster long-term results

Best for those comfortable with delayed gratification.

The Hybrid Approach

Many people combine both:

- Eliminate one small balance for momentum

- Then target high-interest debt

The best strategy is the one you will execute consistently.

Step Four: Control Spending Without Creating Burnout

Reduce Expenses Strategically

Effective cost control focuses on:

- Eliminating inefficiencies

- Cutting low-value spending

- Preserving quality of life

Ask:

“Does this expense move me closer to or further from my goal?”

Avoid Extreme Deprivation

Unsustainable budgets fail.

Debt freedom is achieved through repeatable habits, not temporary suffering.

Step Five: Increase Income Intentionally

Income Acceleration Speeds Debt Reduction

Expense control has limits. Income growth expands capacity.

Options may include:

- Negotiating compensation

- Upskilling for higher-value roles

- Consulting or freelance work

- Monetizing existing expertise

Focus on high-impact income, not constant hustle.

Prevent Lifestyle Inflation

As income rises, redirect additional cash toward:

- Debt elimination

- Emergency savings

- Long-term goals

This discipline shortens the debt timeline dramatically.

The Role of Emergency Savings

Why Savings Matter Even While in Debt

Without a buffer, unexpected expenses create new debt.

Even a modest emergency fund:

- Prevents regression

- Reduces stress

- Protects progress

Stability and debt reduction can coexist.

Common Debt Traps to Avoid

Relying on Consolidation Without Behavior Change

Consolidation can simplify payments, but it does not fix habits.

Without discipline:

- Old debt returns

- New debt accumulates

- Progress stalls

Tools do not replace systems.

Emotional or Stress-Driven Spending

Debt is often reinforced by emotional triggers:

- Stress

- Fatigue

- Social pressure

- Boredom

Awareness is the first line of defense.

Trying to “Catch Up” Too Quickly

Aggressive timelines increase burnout and risk relapse.

Consistency beats intensity.

Applying a CEO Mindset to Debt Elimination

Think Like a Business

Successful organizations:

- Track liabilities

- Manage cash flow

- Set performance metrics

- Review results regularly

Apply the same logic personally.

Measure Progress Consistently

Use:

- Monthly debt balance reviews

- Net-worth tracking

- Cash-flow reports

Visibility drives accountability.

Celebrate Milestones Strategically

Acknowledging progress reinforces discipline and motivation.

Rewards should support—not sabotage—long-term goals.

When Professional Help Makes Sense

Financial Advisors and Credit Counselors

In complex situations, expert guidance can:

- Improve strategy

- Reduce mistakes

- Provide objectivity

Choose professionals who educate and empower.

Legal and Structured Solutions

In severe cases, structured debt solutions may exist. These should be evaluated carefully as part of a broader recovery plan—not as shortcuts.

Life After Debt: What Comes Next

Redirect Freed-Up Cash Flow

Once debt decreases:

- Build emergency reserves

- Invest for the future

- Support meaningful life goals

Debt freedom creates optionality.

Build Long-Term Financial Resilience

Without debt pressure:

- Compounding works in your favor

- Financial stress decreases

- Decision-making improves

Maintain the Systems That Got You There

Debt freedom is maintained through habits, not willpower.

Conclusion

Getting out of debt is not about restriction—it is about regaining control.

With a CEO-friendly approach—focused on clarity, structure, and disciplined execution—debt becomes a solvable problem rather than a permanent burden.

You do not need perfect conditions.

You do not need extreme sacrifice.

You need:

- Clear visibility

- A realistic plan

- Consistent action

Debt does not define your future.

Your decisions do.

Summary:

More often than not, when people take out credit, they believe they are in a good financial position to keep up the monthly repayments on their borrowings, but what happens when something goes wrong and we find ourselves in a difficult debt situation?

Keywords:

get out of debt,debt problem,debt advice,iva,debt management

Article Body:

People can find themselves in debt difficulty for a number of different reasons, but what options are available to resolve a financial issue?

When taking out credit, we generally look at our current financial position and base our repayments on what we can afford according to our current income. We do not tend to look at what could be around the corner.

This more often than not creates immediate risk to us and our families.

Recently a large business in Lincolnshire had to close their doors leaving over 700 people without a job. Suddenly, these people found themselves in a position with no income.

Some of these people will have borrowings with no savings to fall back on; they will now find themselves in a situation where they simply do not have the money to keep up with their financial commitments until they are able to find a new job.

This is just one of the reasons someone kind find themselves in financial difficulty.

Being in a position to some people is unknown territory and they are just not sure where to turn and ask for help.

There are solutions put in place for anyone who finds themselves in position where they no longer repay their debt at the amount set by their agreement.

Your financial position will generally determine which option is suitable when considering ways to resolve a debt problem.

Options available may also depend on whether your borrowing is secured or unsecured.

Generally for personal unsecured debt, options such as a Debt Management Plan may be suitable. Alternatively, if you have a fair amount of income (although it may not be enough to meet current monthly agreed payments) an Individual Voluntary arrangement could be an option.

The most important thing to remember if you ever find yourself in financial difficulty is to make sure your creditors know exactly what is going on.

Some creditors have a bad reputation for being unsympathetic to those who have found themselves in debt difficult. Because of this, some people are afraid to talk to them. Their situation is bad enough without a creditor giving them a hard time over the phone.

The Office of Fair Trading have guidelines that all creditors should abide by, so it is worth reading up on your rights so that if a creditor does work outside of the guidelines, you will recognise this and this will help you inform your creditors you know what rights you have and how you are protected.

If you find it too difficult to talk to your creditors, you can authorise a third party to deal with your debt on your behalf. As long as you have authorised them, your creditors must respect your wishes.

There are a number of financial companies that help people with debt problems. These companies can explain options that available and encourage you not to over commit yourself into anything that may cause more stress.

It is also important to be wary of banks offering refinance. Refinance could be a good option, however, consider the interest you will be paying back on top of what you borrow.

Don�t be tempted by quick fixes, such as borrowing more money, if you know in a few months time you will find yourself back in the same situation.

Regardless of your financial situation, whether you are dealing with personal debt or business debt, there is always a solution. Do not be afraid to seek help and face your debt on. Do not put letters unopened in the bin or in a drawer hidden away.

As long as your creditors are aware of the situation, they can consider whatever proposals are put before them when coming to an agreement on the best way to repay the debt.

Tinggalkan Balasan